Your Corporation Tax must be paid 9 months and 1 day after the end of your accounting period, which is typically your financial year end date.

In your first year of trading, you may have 2 accounting periods, and therefore 2 deadline dates for payments.

Please see the table below:

| Accounting / financial year end date | Latest payment date |

| 31 January | 1 November following |

| 28 February | 1 December following |

| 31 March | 1 January following |

| 30 April | 1 February following |

| 31 May | 1 March following |

| 30 June | 1 April following |

| 31 July | 1 May following |

| 31 August | 1 June following |

| 30 September | 1 July following |

| 31 October | 1 August following |

| 30 November | 1 September following |

| 31 December | 1 October following |

There are a number of ways to find this out:

To create a Business Tax Account (Government Gateway)

For clients of DG Accountancy Services:

There are a number of methods to pay your Corporation Tax bill.

For a full list of options, please refer to HMRC’s official site – https://www.gov.uk/pay-corporation-tax

Our preferred method is to pay via bank transfer from your company bank account using the following bank details:

If you have received your ‘notice to deliver your tax return’ letter from HMRC, it will tell you whether to pay HMRC Shipley or HMRC Cumbernauld.

If you don’t have the letter or are unsure, you should use HMRC Cumbernauld.

Account Name – HMRC Cumbernauld

Account Number – 12001039

Sort Code – 08-32-10

Or

Account Name – HMRC Shipley

Account Number – 12001020

Sort Code – 08-32-10

You will need to use a reference number when making the payment.

There are a number of ways to find this out:

For clients of DG Accountancy Services:

The below is based on the 2024/25 bandings and thresholds:

The main rate of Corporation Tax is 25%, and this is applied to your taxable profits in an accounting period.

If your profits are more than £250,000, you’ll pay the main rate of Corporation Tax on all the profits.

If your profits are £50,000 or less, you’ll pay the small profits rate of 19%

You may be entitled to Marginal Relief if your profits are between £50,000 and £250,000.

The below are purely to give an indication and are by no means to be relied upon, as every situation is slightly different. These are a few case studies to highlight how the Corporation Tax is calculated.

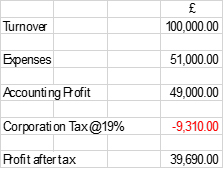

Case Study 1

ABC Recruitment Limited have pre-tax profits of £49,000, there was no entertainment expensed in the year, nor did they acquire any fixed assets. All the assets that they own are fully depreciated.

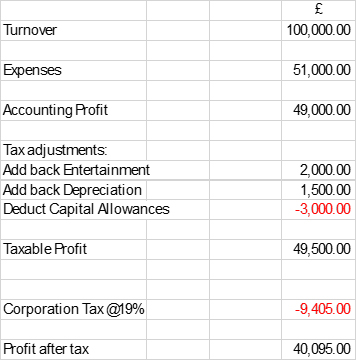

Case Study 2

ABC Recruitment Limited have pre-tax profits of £49,000. Within the £51,000 of expenses, £2,000 was spent on entertainment and there was deprecation expensed of £1,500. They also purchased some new IT equipment (which qualified for Annual Investment Allowance under Capital Allowance rules) totalling £3,000.

Case Study 3

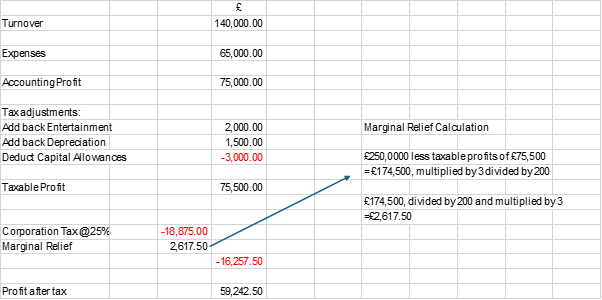

ABC Recruitment Limited have pre tax profits of £75,000. Within the £65,000 of expenses, £2,000 was spent on entertainment and there was deprecation expensed of £1,500. They also purchased some new IT equipment (which qualified for Annual Investment Allowance under Capital Allowance rules) totalling £3,000.

Case Study 4

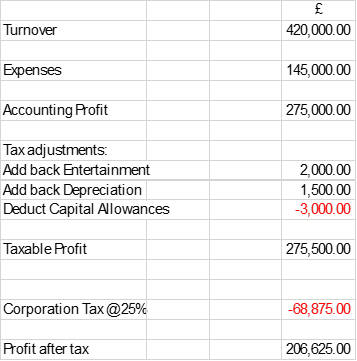

ABC Recruitment Limited have pre tax profits of £275,000. Within the £65,000 of expenses, £2,000 was spent on entertainment and there was deprecation expensed of £1,500. They also purchased some new IT equipment (which qualified for Annual Investment Allowance under Capital Allowance rules) totalling £3,000.

For a more detailed explanation, please visit HMRC on https://www.gov.uk/corporation-tax-rates

The key date for payment of your personal tax bill is 31st January each year.

For example, for the tax year covering 6th April 2022 to 5th April 2023, the tax return must be filed and any tax payments would need to be submitted by 31st January 2024.

If your tax bill is over £1,000, then you may be required to make payments on account, which means you will also need to make payments on 31st July each year too.

There are a number of ways to find this out:

For clients of DG Accountancy Services:

There are a number of methods to pay your personal tax bill.

For a full list of options, please refer to HMRC’s official site – https://www.gov.uk/pay-self-assessment-tax-bill

Our preferred method is to pay via bank transfer from your bank account using the following bank details:

You can use either of the following:

Account Name – HMRC Cumbernauld

Account Number – 12001039

Sort Code – 08-32-10

Or

Account Name – HMRC Shipley

Account Number – 12001020

Sort Code – 08-32-10

The reference you should use when making payment of your personal tax bill is your Unique Tax Reference Number (UTR) followed by a K, to make it into an 11 digit reference.

For example:

If your reference is 12345 67890, then the reference you would use would be 1234567890K

You can find your UTR number in a variety of places:

Sole Traders, Employees and Landlords

The below is relevant for the 2024/25 tax year and applies to sole traders, employees and landlords. This is taxed under Income Tax rules.

Typically, all UK residents will receive a personal allowance of £12,570, this means that you don’t pay any tax on the first £12,570 of your earnings.

Your business expenses (those that are allowable for deduction), will be deducted from your business income to arrive at your business profits.

After adjusting for items such as capital allowances, you then arrive at your total income.

You take off your personal allowance to arrive at your taxable income.

The first £37,700 of the taxable income will be taxed at 20%. This takes you up to £50,270. This is the Basic Rate of Tax banding (BRT)

From £50,271 to £125,140 is the Higher Rate of Tax banding (HRT). This band is taxed at 40%.

Please note that when your total income reaches £100,000 you will start to lose your personal allowance at a rate of £1 for every £2 you earn over the £100,000 mark.

Income over £125,140 is taxed at the additional rate of tax which is 45%.

| Band | Taxable Income | Tax Rate |

| Personal Allowance | Up to £12,570 | 0% |

| Basic Rate | £12,571 to £50,270 | 20% |

| Higher Rate | £51,271 to £125,140 | 40% |

| Additional Rate | Over £125,140 | 45% |

Those who are sole traders will also need to pay Class 4 National Insurance at the following rates:

| Band | NI’able Income | Tax Rate |

| Up to Lower Profits Limit | Up to £12,570 | 0% |

| Between Lower and Upper Profits Limit | £12,571 to £50,270 | 6% |

| Over Upper Profits Limit | Over £51,271 | 2% |

Limited Company Directors/Shareholders

The below is relevant for the 2024/25 tax year and applies to owner managed business directors and recipients of dividends. This is taxed under Income Tax and Dividend Tax rules.

Typically, all UK residents will receive a personal allowance of £12,570, this means that you don’t pay any tax on the first £12,570 of your earnings.

Typically, directors of owner managed businesses will be on a low salary/high dividend strategy.

The level of salary taken by the director will be dependent on whether there are employees on the payroll or whether there is more than 1 director.

If we assume that there is one director who receives total income of £60,000, with the first £9,096 being PAYE income with the balance made up of dividends.

You take off your personal allowance to arrive at your taxable income.

The next £500 is also tax free as is covered by a dividend allowance.

The first £37,200 of the taxable income will be taxed at 8.75%. This takes you up to £50,270. This is the Basic Rate of Tax banding (BRT)

From £50,271 to £125,140 is the Higher Rate of Tax banding (HRT). This band is taxed at 33.75%.

In the example above £37,200 will be taxed at 8.75% and £9,729 will be taxed at 33.75%

Please note that when your total income reaches £100,000 you will start to lose your personal allowance at a rate of £1 for every £2 you earn over the £100,000 mark.

Income over £125,140 is taxed at the additional rate of tax which is 39.35%.

| Band | Taxable Income | Tax Rate |

| Personal Allowance | Up to £12,570 | 0% |

| Dividend Allowance | £12,571 to £13,070 | 0% |

| Basic Rate | £13,071 to £50,270 | 8.75% |

| Higher Rate | £51,271 to £125,140 | 33.75% |

| Additional Rate | Over £125,140 | 39.35% |

There is no National Insurance to pay on dividend income.

For a full list of tax and national insurance rates and thresholds see:

Income Tax – https://www.gov.uk/income-tax-rates

Dividend Tax – https://www.gov.uk/tax-on-dividends

National Insurance – https://www.gov.uk/government/publications/rates-and-allowances-national-insurance-contributions/rates-and-allowances-national-insurance-contributions#class-1-national-insurance-thresholds

When you are in the self assessment system and your annual liability hits £1,000, you will need to start making payments on account.

A basic illustration follows:

Tax Year: 2021/2022

Liability : £2,000

Payments as follows:

| Payment Date | Amount | Reason |

| 31 January 2023 | £2,000 | Your liability |

| 31 January 2023 | £1,000 | Payment on Account 1 (towards the 2022/23 tax bill) |

| 31 July 2023 | £1,000 | Payment on Account 2 (towards the 2022/23 tax bill) |

Therefore, at this stage, you have paid all of your 2021/22 tax bill and made payments on account of £2,000 towards your 2022/23 tax bill.

Payments on account work on the assumption that next year, you will earn the same as in the past year and therefore 2 x 50% payments are made.

Tax Year: 2022/23

Liability: £5,000

Payments as follows:

| Payment Date | Amount | Reason |

| 31 January 2024 | £3,000 | This is the balancing payment, your liability less the payments on account made. |

| 31 January 2024 | £2,500 | Payment on Account 1 (towards the 2023/24 tax bill) |

| 31 July 2024 | £2,500 | Payment on Account 2 (towards the 2023/24 tax bill) |

Therefore, at this stage, you have paid all of your 2022/23 tax bill and made payments on account of £5,000 towards your 2023/24 tax bill.

If you know that your income is going to decrease in the following year for whatever reason, there is an opportunity to reduce your payments on account to reflect the predicted tax liability in the following year.

You have 1 month and 7 days to make payment of your VAT bill after your VAT quarter has ended.

Please see the table below:

| VAT quarter end date | Latest payment date |

| 31 January | 7 March |

| 28 February | 7 April |

| 31 March | 7 May |

| 30 April | 7 June |

| 31 May | 7 July |

| 30 June | 7 August |

| 31 July | 7 September |

| 31 August | 7 October |

| 30 September | 7 November |

| 31 October | 7 December |

| 30 November | 7 January |

| 31 December | 7 February |

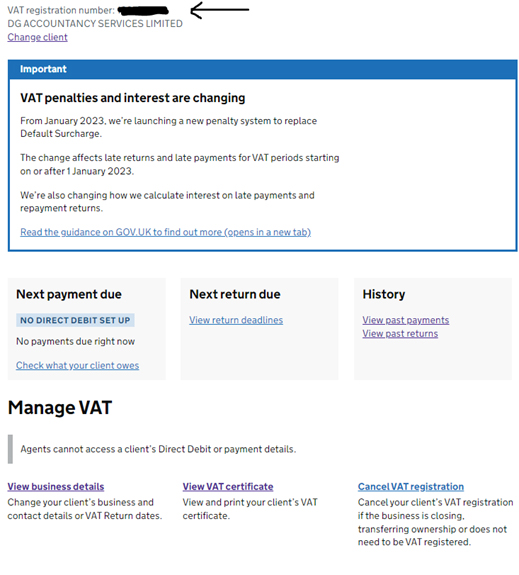

There are a number of ways to find this out:

For clients of DG Accountancy Services:

The liability will be the Box 5 number on your return

There are a number of methods to pay your VAT bill.

For a full list of options, please refer to HMRC’s official site – https://www.gov.uk/pay-vat

Our preferred method is to pay via bank transfer from your bank account using the following bank details:

You can use either of the following:

Account Name – HMRC VAT

Account Number – 11963155

Sort Code – 08-32-00

The reference to use when paying your VAT bill is your VAT reference number, it is a 9 digit number.

You can find this in a variety of places:

From April 2024, the registration threshold for mandatory VAT registration is £90,000 (previously £85,000) of income for any 12 consecutive months.

There is a common misconception that the 12 month period is either a calendar year or the financial year. This is not the case, it needs to be assessed each month on a 12 month rolling basis.

There is nothing preventing a business that is billing under £90,000 from voluntarily registering for VAT if the circumstances suit them.

Businesses can deregister from VAT. The deregistration threshold is set at £88,000 (previously £83,000). The are specific circumstances that need to be met when deregistering, so contact us if you wish to deregister and we can guide you on the process.

For more information on VAT, please visit https://www.gov.uk/register-for-vat

This depends on whether you pay your PAYE liability monthly or quarterly.

Please see the tables below:

Monthly

| PAYE periods ending between | Latest payment date |

| 6 April and 5 May | 22 May |

| 6 May and 5 June | 22 June |

| 6 June and 5 July | 22 July |

| 6 July and 5 August | 22 August |

| 6 August and 5 September | 22 September |

| 6 September and 5 October | 22 October |

| 6 October and 5 November | 22 November |

| 6 November and 5 December | 22 December |

| 6 December and 5 January | 22 January |

| 6 January and 5 February | 22 February |

| 6 February and 5 March | 22 March |

| 6 March and 5 April | 22 April |

Quarterly

| PAYE periods for the following quarters | Latest payment date |

| 6 April and 5 July | 22 July |

| 6 July and 5 October | 22 October |

| 6 October and 5 January | 22 January |

| 6 January and 5 April | 22 April |

There are a number of ways to find this out:

You can extract the amounts from your payroll reports, however you may wish to read “What makes up my PAYE liability?” prior to doing so.

There are a number of methods to pay your PAYE bill.

For a full list of options, please refer to HMRC’s official site – https://www.gov.uk/pay-paye-tax

Our preferred method is to pay via bank transfer from your bank account using the following bank details:

You can use either of the following:

Account Name HMRC – Cumbernauld

Account Number – 12001039

Sort Code – 08-32-10

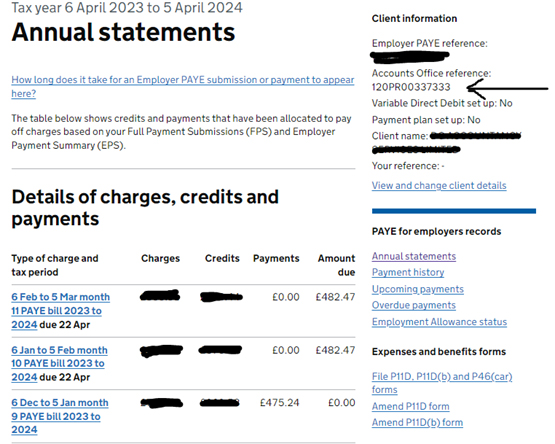

You should use your 13 digit Accounts Office Reference number, it will start with 3 Numbers, followed by 2 Letters and then another 8 numbers, such as below:

120AB12345678

There are a number of ways to find this out:

The PAYE bill is a combination of things such as:

There are other items that could fall into this list, but the above are the most common items.

Employment Allowance

Qualifying employers receive (in 2024/25) a £5,000 Employment Allowance, which means the first £5,000 of calculated Employers National Insurance does not have to be paid to HMRC.

A Government Gateway Account is an area on the Gov.uk website where you can access your personal or business information.

Individuals will require a Personal Tax account and businesses will need a Business Tax Account.

What can I access in a Personal Tax Account?

Amongst other things:

What can I access in a Business Tax Account?

Amongst other things:

Personal Tax Account

You can create a Personal Tax Account by following the below link:

https://www.gov.uk/personal-tax-account

Business Tax Account

You can create a Personal Tax Account by following the below link:

https://www.gov.uk/guidance/sign-in-to-your-hmrc-business-tax-account

Once you have your account set up, you will need to add the services that are applicable to your business.

Simply go to “Add Service/Tax” and find the tax from the list.

Some will allow instant access, some will require a code to be posted to you before you can fully use this part of the system.

Corporation Tax

PAYE

CIS

VAT

These will be the main services clients will add.

If you are looking to obtain a mortgage or are remortgaging, your broker is likely to ask you for SA302 or Tax Year Overviews.

The SA302 is a form produced by HMRC which is effectively your Tax Computation printed on HMRC headed paper.

HMRC are and have been for some time phasing these out, and have built a function within the personal tax account for you to download ‘Tax Year Overviews’. These will sit alongside the Tax Computation produced when completing your tax return.

The Tax Computation (which you can download from Onvio) coupled with the Tax Year Overview, replaces the old SA302.

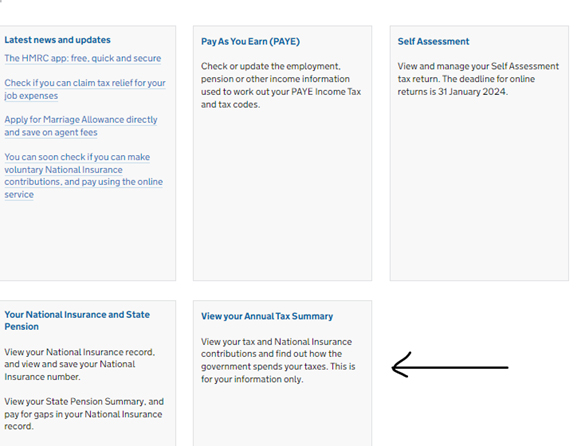

To download your Tax Year Overview, you will need to log into your Personal Tax Account

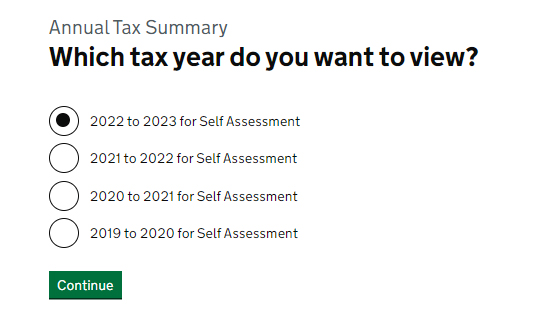

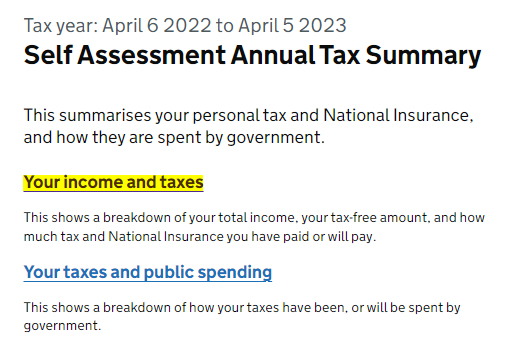

Once logged in, you will need to select View Your Annual Tax Summary from the options as below:

Select the year you require:

Select – Your Income and Taxes

You will then be displayed with a screen covering your total income and the tax paid which should agree to the Tax Computation prepared by us and held on Onvio.

To save this screen click on the icon

Onvio Client Centre (by Thomson Reuters) is essentially a cloud based electronic file storage system that DG Accountancy Services use to store all of our files on.

Many people will have heard of Dropbox or One Drive, Onvio Client Centre performs the same functionality.

Additional features that are available on Onvio Client Centre, are the ability to share folders with other clients and the e-signature functionality.

Upon becoming a client, you will be invited to create an account on the portal via an email invitation.

Once you have created your account and once a document has been added to the shared folder, you will receive an email alerting you that we have shared a document.

Within the email, there will be a link to take you straight into the document(s) we have shared with you.

You can also access Onvio Client Centre from the Client Zone on our website:

www.businesstaxaccountants.co.uk

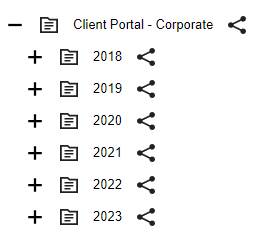

We keep the structure of the folders fairly simple:

The year coordinates with a year end, so for sole traders, the 2023 folder will contain the 2022/23 tax documents and for Limited Companies, if your year end is say 30 April 2023, then your accounts and tax documents will be filed in the 2023 folder.

![]() means that this is a shared client folder.

means that this is a shared client folder.

Within Onvio Client Centre, you will always only have 1 log in, but if you are a Limited Company owner, you may have 2 profiles within the account, one for the company and one for you personally.

Company documents will be stored in the company profile and personal tax documents in your personal one.

You can toggle between profiles by clicking on the dropdown arrow as indicated above.

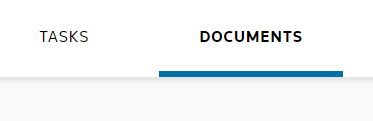

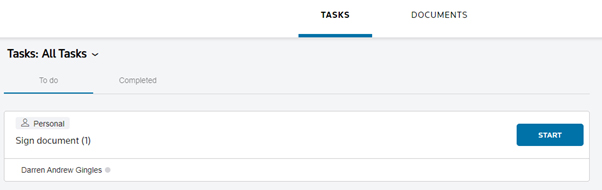

Across the top you will have 2 areas within the profiles, Documents and Tasks

All documents are held under the Documents tab, and when you are required to provide an e-signature, these will be listed under Tasks as shown below:

Please note that you will also need to be in your personal profile to see the tasks, the e-signature request is sent to the individual, not the company, hence why it sits in the personal profile rather than the business profile.

This is fairly common. When you set up the 2 Factor Authentication, you will have the chance to download a number of temporary access codes for this kind of situation, then when asked for the 2FA code, you can use one of the codes on the list, and then once logged in, you can access the QR code to link your new phone up to Onvio Client Centre.

If you do not have a list of temporary access codes, DG Accountancy Services can create one for you which has a 24 hour validity. Please email your primary contact for this if the situation arises.

After you have this code follow these steps:

To register a new device:

Download the Authenticator App from the App Store or Google Play on your new device.

Follow the instructions to pair your new device with Onvio Client Centre.